Newsletters

The 2024 State Budget Law came into force on 1 January 2024 and introduced the following amendments to the Personal Income Tax Code and related legislation:

🔸 Repeal of the non-habitual residents regime (NHR): click HERE for more information on this amendment;

🔸 New Former Residents Programme [Programa "Ex-Residentes"]: click HERE for more information on this amendment;

🔸 "Tax incentives for scientific research and innovation": click HERE for more information on this amendment;

🔸 Amendments to the regime applicable to the taxation of gains derived from stock options plans: click HERE for more information on this amendment;

🔸 Allowances and compensation for travels in own car: the rule that reduced the amount of allowances and compensation for travel in own car originally provided for civil servants was repealed. The following amounts shall then be reinstated:

- travels in own car: the value of € 0.36 shall be increased to € 0.40 per kilometre;

- travels in Portugal:

- workers: the amount of € 50.20 shall be increased to € 62.75;

- members of the Government and equivalent in the private sector: the amount remains at €69.19, as it has not been reduced.

- travels abroad:

- workers: the amount of € 89.35 shall be increased to € 148.91;

- members of the Government and equivalent in the private sector: the amount of € 100.24 shall be increased to € 167.07.

🔸 Profit-sharing: exemption up to a limit of five times the amount proposed for the minimum guaranteed monthly salary for amounts paid to employees as profit-sharing in companies, by way of a balance-sheet bonus, paid by entities whose average nominal valuation of fixed remuneration per employee in 2024 is equal to or greater than 5%.

🔸 Tax incentive for workers' housing: Income from work in kind resulting from the use of a permanent house located in Portugal, provided by the employer, for the period between 1 January 2024 and 31 December 2026, shall be exempted from personal income tax and social contributions (provided all other requirements are met).

🔸 IRS Jovem (Taxtion of Personal Income Tax of Young Professionals): The amounts of the exemptions provided for in this scheme are updated as follows:

- 100% in the first year up of 40 times the value of the IAS;

- 75% in the second year up to 30 times the value of the IAS;

- 50% in the third and fourth years up to 20 times the IAS value;

- 25% in the final year up to 10 times the value of the IAS.

🔸 30% of the amount spent on professional training is now deductible from personal income tax, as training and education expenses, by any member of the household, up to the an amount of €800.

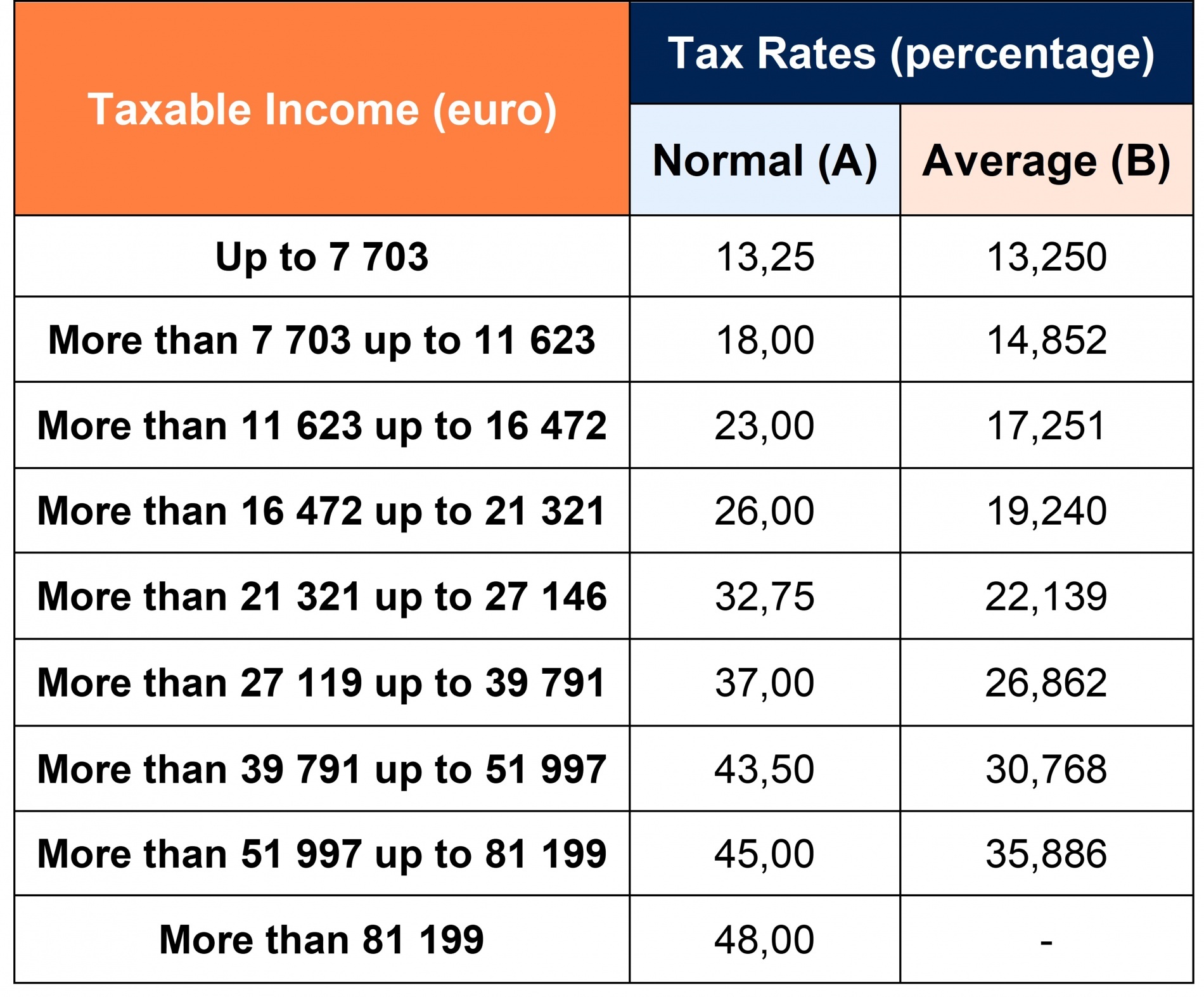

🔸 Changes to the marginal rates applicable to the overall taxable income. The new table in force shall be as follows: